Call us on

0113 403 5584

info hub

Later Life

Lending Explained

Later Life Lending Options

Lending options tailored to your specific needs, to help you make the right choice

Various fixed rate periods available.

Tax free capital.

No repayment options.

Borrow from 10k / no maximum limit.

Various fixed rate periods available.

Tax free capital.

No repayment options.

Borrow from 10k / no maximum limit.

Later Life

Lending Options

What is Equity Release?

Releasing equity from your home is a significant financial decision and one not to be taken without conducting your own research. Take a look, below, at some of the most common questions that customers ask our equity release advisers.

Lifetime mortgage

You would need to be 55 to qualify for this type of plan. A Lifetime mortgage is always taken out on the main residence. You continue to own your home.

The mortgage borrowing is not assessed by a lender on your income amount, although we will ask questions about income to provide robust advice. You can move in future subject to terms and conditions of each lender.

The amount provided through a lifetime mortgage product is calculated against a clients age and if joint borrowers the youngest clients’ age. The lender will use age, the valuation of the property and in some cases health to provide the amount of permitted lending. There is no upper age limit to taking out these types of plans.

Historically Lifetime mortgages were wholly accumulated interest mortgages, which mean they rolled up for the lifetime of the loan. New product innovation sees this product offer payment options to service & control interest costs.

This product has a no negative equity guarantee so you will never leave a debt to your beneficiaries.

This type of plan provides a drawdown facility to support future ongoing borrowing. You will not be charged set up costs every time you wish to draw funds from the agreed facility.

This type of plan has been proven to save interest costs over the years. These types of mortgages are portable which means you can transfer from one property to another.

The lender would review the request & the acceptance would be lender dependent on how much you had originally borrowed. If you move to a smaller value property, you may have to repay a portion of the lending to bring the loan ratio inline with the new lower value property.

Residential & Later Life Mortgages

These plans are typically available from age 50, this is a changing world, as lenders return to the retirement sector & drive more lending options for you. This may be news to you, but traditional lenders do still deal with clients like you. We have experience of helping clients to find these options.

The available lending amount on this type of mortgage borrowing is typically based on the amount of income you will have approaching retirement or in retirement.

In some cases, lender calculations will consider assets such as pension fund values, investment portfolios, other income from land & property & asset values such as other property. The lenders look for proof that a mortgage can be afforded now and, in the future, looking at future income provisions and a much more detailed review of finances is taken out.

We have been able to find beneficial interest rate offers on these products especially for people in the age 50 to 60 age range, some of these lender options will run to age 80. Some options have a lifetime term.

Traditional lenders may need to see how you will repay the mortgage at the end of the term. Retirement Interest only providers will let you retain the borrowing for a lifetime.

These types of mortgages normally have a reviewable interest rate every 2 – 5 years and can be offered on fixed, lifetime fixed or variable interest rates.

This type of mortgage does not offer a drawdown facility for ongoing borrowing needs. You could however take a further advance with a new assessment, subject to the lender.

The key differences to consider

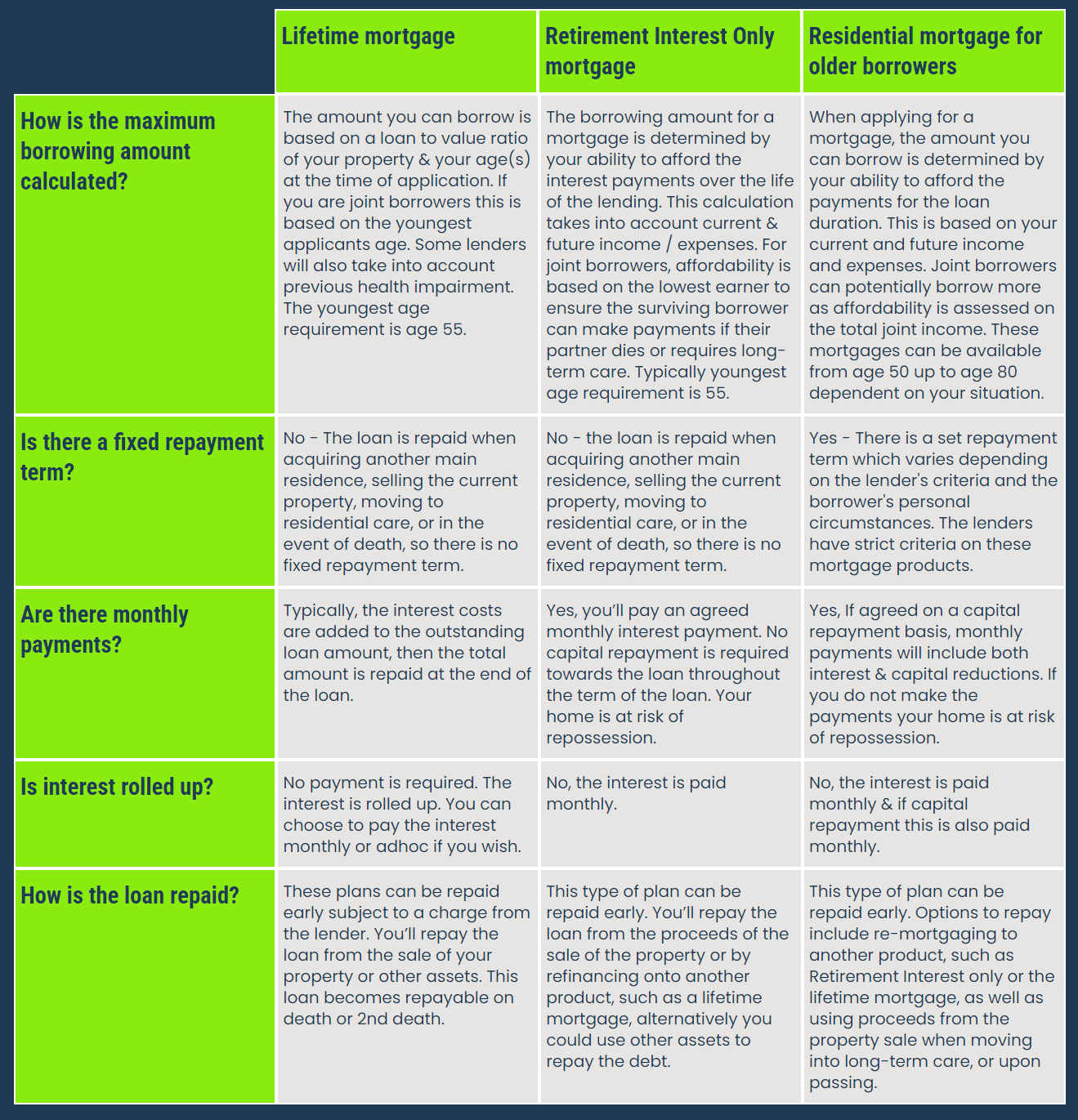

Lifetime mortgage

Retirement Interest Only mortgage

Residential mortgage for older borrowers

How is the maximum borrowing amount calculated?

The amount you can borrow is based on a loan to value ratio of your property & your age(s) at the time of application. If you are joint borrowers this is based on the youngest applicants age. Some lenders will also take into account previous health impairment. The youngest age requirement is age 55.

The borrowing amount for a mortgage is determined by your ability to afford the interest payments over the life of the lending. This calculation takes into account current & future income / expenses. For joint borrowers, affordability is based on the lowest earner to ensure the surviving borrower can make payments if their partner dies or requires long-term care. Typically youngest age requirement is 55.

When applying for a mortgage, the amount you can borrow is determined by your ability to afford the payments for the loan duration. This is based on your current and future income and expenses. Joint borrowers can potentially borrow more as affordability is assessed on the total joint income. These mortgages can be available from age 50 up to age 80 dependent on your situation.

Is there a fixed repayment term?

No - The loan is repaid when acquiring another main residence, selling the current property, moving to residential care, or in the event of death, so there is no fixed repayment term.

No - the loan is repaid when acquiring another main residence, selling the current property, moving to residential care, or in the event of death, so there is no fixed repayment term.

Yes - There is a set repayment term which varies depending on the lender's criteria and the borrower's personal circumstances. The lenders have strict criteria on these mortgage products.

Are there monthly payments?

Typically, the interest costs are added to the outstanding loan amount, then the total amount is repaid at the end of the loan.

Yes, you’ll pay an agreed monthly interest payment. No capital repayment is required towards the loan throughout the term of the loan. Your home is at risk of repossession.

Yes, If agreed on a capital repayment basis, monthly payments will include both interest & capital reductions. If you do not make the payments your home is at risk of repossession.

Is interest rolled up?

No payment is required. The interest is rolled up. You can choose to pay the interest monthly or adhoc if you wish.

No, the interest is paid monthly.

No, the interest is paid monthly & if capital repayment this is also paid monthly.

How is the loan repaid?

These plans can be repaid early subject to a charge from the lender. You’ll repay the loan from the sale of your property or other assets. This loan becomes repayable on death or 2nd death.

This type of plan can be repaid early. You’ll repay the loan from the proceeds of the sale of the property or by refinancing onto another product, such as a lifetime mortgage, alternatively you could use other assets to repay the debt.

This type of plan can be repaid early. Options to repay include re-mortgaging to another product, such as Retirement Interest only or the lifetime mortgage, as well as using proceeds from the property sale when moving into long-term care, or upon passing.

What are the benefits and drawbacks of equity release?

Benefits

Unlock tax-free funds from your home

Retain full home ownership

Option to make reduced or no monthly repayments

Never owe more than your home's worth

Re-mortgage in the future (not guaranteed and may be subject to early repayment charges)

Drawbacks

The amount you owe grows quickly due to compound interest

It will reduce your estate's value and may affect entitlement to means-tested benefits

It may leave you with limited or no property equity

It will reduce your future financial options

It's a long-term financial product, usually repaid when the last borrower dies or enters long-term care (or early repayment charges may apply)

Why do clients utilise Later Life Lending?

Pay off an existing mortgage

I frequently assist clients that have reached the end of their mortgage term, and have no other option to consider other than sale, but they wish to remain in their home.

In some cases, I also find that our clients are unable to afford the mortgage on their home, there are no other cheaper mortgage options and they do not wish to move. In this scenario, a later life borrowing option can be a suitable option.

Fund & enjoy holidays

I deal with a large majority of clients that wish to utilise funds to enjoy their life. They wish to travel to the places they love or in fact to explore new places. This is sometimes a decision they make following the loss of a loved one as they its now they wish to enjoy the day they’ve been blessed with, alternatively they’ve worked hard all their life and wish to enjoy some well-deserved relaxation.

Home improvements

This is one of the most popular uses of later life lending.

Do you wish to add an extension or replace the conservatory to enjoy the extra living space? Its possible this type of borrowing could help you.

One of our clients had recently been declined for a grant to upgrade her bathroom to a shower room, so she utilised a later life lending option to achieve her goal, she said the upgrade to her house – would now make it old age proof!

Repaying personal loan

and credit cards

You may have a situation whereby you wish to reduce your outgoings on debts to enrich your life; with correct advice a later life lending option could be the solution for you.

New Car & Medical reasons

For some of our clients, a new car is high up on the list of things that they would do with the money raised. We recently had a lady jump the NHS que to have her new knees completed and now she is already up and about enjoying life again, she is unable to put a price on this outcome.

Purchasing a new home

I recently helped a lady of 70 upsize her property so that she had more room in the house for family get togethers. I’ve also supported many of these cases & have a huge wealth of experience in this type of transaction, this experience in turn would help you manage the transaction smoothly.

Inheritance tax planning

and gifts to family

Some of our clients have utilised Later life lending to reduce their inheritance tax bill. To understand how this would work for you, i can provider a referral to an inheritance tax specialist. Releasing property wealth and gifting to family is one way of reducing your estate value.

Gifts to family could help them gain a foot on the property ladder. We have helped many people provide gifts to their family.

A recent client even paid for his daughters wedding day with a Lifetime mortgage.

Increase or top up income

As we see the state pension slip away, every time you get that bit closer to that golden retirement date, some of our recent clients have opted to use Later life lending to top up their income due to pension income gaps.

I have also seen an uptake in clients using later life lending options due to tax implications attached to drawing their pension funds from a drawdown type situation. This can have tax advantages.

We always recommend you seek advice from a pension specialist and we can provide a referral for this advice.

Purchase a holiday home or caravan

I’ve personally dealt with many clients who have health impairment and they had been recommended to move into long term care, with careful planning & advice these clients accessed later life lending options and spent their twilight years in the comfort of their own home, with their own personal care.

Equity release can come with potential risks and consequences, professional advice should always be sought before advancing.

Not ready to contact us? Here are some of our FAQs

Releasing equity from your home is a significant financial decision and one not to be taken without conducting your own research. Take a look, below, at some of the most common questions that customers ask our equity release advisers.

How does equity release work?

Equity release enables UK homeowners aged 55 and over to access tax-free cash from their home's value, with lifetime mortgages being one of the most popular options.

The amount you can borrow is based on the age of the youngest applicant and the value of your property. Factors like health conditions and property postcode can also influence the loan size.

The FCA mandates that you receive specialist advice, requiring you to have both a financial adviser and a legal representative. Lenders charge a fixed interest rate over your lifetime.

You have the option to make payments to the lender, which will affect your future mortgage balance.

The released funds can be received as a one-off payment or through a series of ad-hoc lump sums, known as drawdown.

Finally, the lender secures the loan by placing a first legal charge on your property.

How much equity can I release from my property?

The amount you can borrow through equity release depends on the scheme type, your age, and your property's value. We recommend borrowing only what you need to minimize interest rates.

For lifetime mortgages, the minimum loan starts at £10,000. At age 55, you can release up to 33% of your property's value, increasing to up to 60% by age 83. Home reversion schemes start with a minimum loan of £25,000, allowing you to sell up to 100% of your home's value at a discounted rate.

Retirement Interest Only mortgages (RIOs) begin at age 50 and offer borrowing capacity similar to residential mortgages, based on affordability. Your pre- and post-retirement income and credit record will determine the maximum amount you can release with a RIO.

For a quick estimate, try our Equity Release Calculator.

Is equity release safe?

Equity release offers numerous safeguards. However, it is important to understand that equity release can impact means-tested benefits and reduce the equity you may leave to your beneficiaries. Therefore, consider all your options, including downsizing, before making a decision.

If you're thinking about equity release, thoroughly research the company providing the advice, including customer reviews. At Search Equity Release, we've been offering impartial, whole-of-the-market advice on equity release and retirement mortgages.

Modern equity release schemes include features that ensure full protection for homeowners.

Firstly, the no negative equity guarantee ensures that beneficiaries will never owe more to the equity release company than the property's sale value.

Additionally, for joint applicants, there is an option for a 3-year no early repayment charge (ERC). This allows you to repay the loan without penalty within three years following the death or long-term care of a partner.

Am I eligible for equity release?

To qualify for equity release, you must meet the following criteria:

- Be a UK resident aged 55 or over.

- Own 100% of your residential property.

- Have a property with a minimum valuation of £70,000.

If you have an existing mortgage, it must be repaid either before or upon completion of your equity release plan. This can be done using your own funds or from the proceeds of the equity release itself.

Is my property eligible for equity release?

To qualify for equity release, your property must be your main residence and located in England, Scotland, Wales, or Northern Ireland.

Typically, the property needs to be of standard construction with a minimum value of £70,000. While different lenders have various maximum property values, amounts up to £10 million are common, with some companies offering unlimited maximum property value ceilings.

Both freehold and leasehold houses are eligible, while lending on leasehold flats and maisonettes is also allowed. Lease terms must generally exceed 75 years to meet lending criteria.

The property should have no constraints on residential use. Unusual features, such as annexes, large acreage, trusts, or non-standard build types, usually require a lender referral.

Equity Release (Lifetime Mortgage) is a loan secured against your home. To understand the features and risks of equity release, please ask for a personalised illustration.

As a whole-of-market firm, we continue to offer a comprehensive range of equity release (lifetime mortgages) products from across the market.

If you are thinking of consolidating existing borrowing, you should be aware that you may be extending the term of the debt and increasing the total amount you repay.

The actual interest rate and fees charged will depend upon your circumstances.

Unless you decide to go ahead, our service is at our cost. Only if your case completes would our advice fee of a maximum of £1,495 be payable. Other lender & solicitor fees may apply.

Equity release may reduce the value of your estate and could affect your entitlement to means-tested benefits.

At One Stop 4 Equity Release Limited we are committed to providing our clients with expert later life financial advice tailored to their individual needs.

However, for Retirement Interest-Only (RIO) Mortgages, Term Interest-Only (TIO) Mortgages, and Fixed Rate Later Life Mortgages, we have chosen to work exclusively with LiveMore Mortgages. This means that while we consider all available equity release and later life lending options across multiple providers, for these specific products, we will only recommend solutions from LiveMore Mortgages.

If you proceed with a mortgage that requires payments to be made, your home maybe repossessed if you do not keep up repayments on your mortgage.

Search Equity Release is a trading style of One Stop 4 Equity Release Limited, One Stop 4 Equity Release Limited is authorised and regulated by the Financial Conduct Authority under No: 952887. One Stop 4 Equity Release Limited is a registered company in England and Wales, registration No: 13452621. Registered address: 30 North Street, Bourne, PE10 9AB.

Important: The information on this page is based on draft legislation and may be subject to change.

Search Equity Release © 2024 | All Rights Reserved | Privacy Notice | Complaints Policy | Vulnerable Consumer Policy | Regulatory Statement